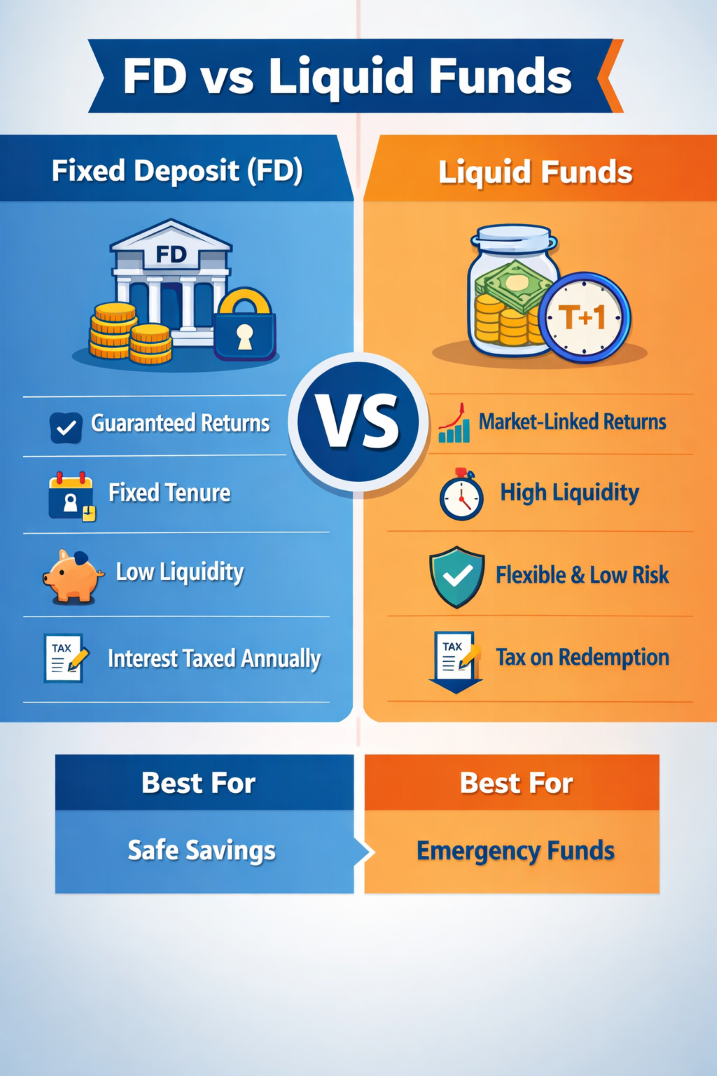

📌 FD vs Liquid Funds: Which is Better for You?

Fixed Deposits (FDs) and Liquid Funds are both popular options for short-term savings. FDs offer guaranteed returns with fixed tenure, while Liquid Funds provide flexibility and market-linked yields. The right choice depends on your need for certainty versus accessibility.

🔎 What is a Fixed Deposit (FD)?

- Definition: A lump-sum deposit with a bank for a fixed tenure.

- Returns: Guaranteed interest rate, unaffected by market changes.

- Tenure: 7 days to 10 years.

- Withdrawal: Premature withdrawal attracts penalties (0.5–1% lower interest).

- Safety: Bank FDs insured up to ₹5 lakh by DICGC. Company/NBFC FDs are not insured.

🔎 What is a Liquid Fund?

- Definition: A debt mutual fund investing in short-term instruments (maturity ≤ 91 days).

- Returns: Market-linked, not guaranteed.

- Tenure: No lock-in; redeem anytime.

- Liquidity: T+1 settlement, with instant redemption up to ₹50,000 or 90% of folio value.

- Safety: Diversified holdings, regulated by SEBI.

📊 FD vs Liquid Funds – Key Differences

| Feature | Fixed Deposit (FD) | Liquid Fund |

|---|---|---|

| Returns | Fixed & guaranteed | Market-linked, not guaranteed |

| Liquidity | Moderate (penalty on early withdrawal) | High (T+1 or instant redemption) |

| Risk | Very low (insured up to ₹5 lakh) | Low (credit & interest rate risk) |

| Taxation | Interest taxed annually at slab rate | Gains taxed at slab rate on redemption |

| Flexibility | Low | High |

| Best For | Risk-averse savers | Emergency funds & idle cash |

⚖️ Safety Comparison

- FDs: Safer due to deposit insurance (₹5 lakh cap).

- Liquid Funds: No insurance, but diversification and SEBI regulation reduce risk.

💰 Returns Comparison

- FDs: Predictable, fixed rate.

- Liquid Funds: Yields fluctuate with interest rate cycles. Better in rising-rate environments.

🏦 Taxation

- FDs: Interest taxed annually, TDS applicable.

- Liquid Funds: Gains taxed at slab rate only on redemption (defers tax liability).

🚨 Risks to Consider

- FDs: Inflation risk, reinvestment risk, premature withdrawal penalty.

- Liquid Funds: Credit risk, NAV fluctuations, market-linked returns.

✅ When to Choose FD

- You want guaranteed returns.

- You have a fixed investment horizon.

- You prefer safety over flexibility.

✅ When to Choose Liquid Fund

- You need quick access to money.

- You’re building an emergency fund.

- You want better yields than a savings account.

🏁 Final Thoughts

FDs prioritize certainty, while Liquid Funds prioritize flexibility. Many smart investors use both — FDs for locked-away savings and Liquid Funds for emergency or idle cash.